How Can Construction Companies Maximize Vehicle Tax Deductions in 2026?

In Brief:

Section 179 lets construction companies deduct the full purchase price of qualifyin…

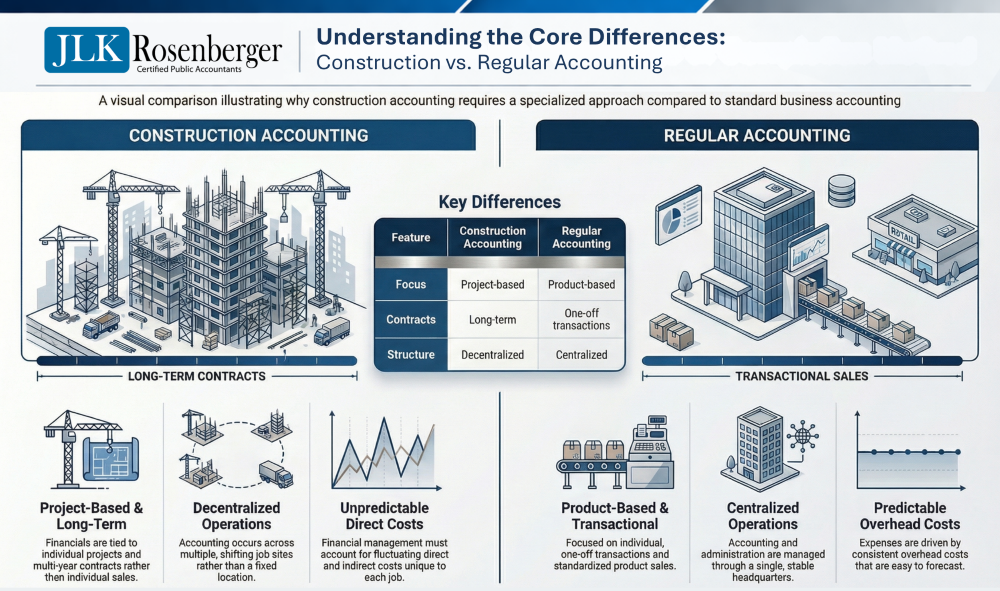

Construction accounting differs fundamentally from general business accounting because contractors operate in a project-driven environment where revenue, costs, and cash flow are tied to long-term contracts rather than recurring sales cycles. Each project functions as its own profit center with unique timelines, risk profiles, and cost structures. Financial performance must be tracked at the job level, often across months or years, while revenue is recognized based on progress toward completion rather than simple invoicing. This creates complexities around work-in-progress reporting, retainage, and percentage-of-completion revenue recognition that do not exist in most other industries.

The construction model also introduces financial risks that are far less common in traditional businesses. Long-term contracts expose contractors to estimating errors, labor and material volatility, weather delays, subcontractor performance issues, and scope changes that can erode margins over time. Retainage withholds a portion of earned revenue until project completion, creating persistent cash flow pressure even on profitable jobs. Change orders and claims may alter project economics but are often approved or collected months after costs are incurred. Cost overruns, inaccurate job costing, or delayed billing can quickly convert profitable work into losses if not identified early through disciplined financial monitoring. Because multiple projects run simultaneously, these risks compound across the portfolio, making accurate project-level accounting essential to overall company performance.

Specialized construction CPAs help contractors manage these complexities and grow profitably by aligning accounting systems, financial reporting, and operational decision-making with how construction businesses actually generate profit. They implement job costing structures that reveal true project margins, develop reliable work-in-progress reporting to detect margin fade early, and ensure revenue recognition reflects economic reality. Beyond compliance, construction-focused advisors analyze estimating accuracy, overhead recovery, and project mix to improve bidding and pricing strategies. They also optimize tax methods, strengthen bonding capacity, and support cash flow planning so contractors can take on larger projects with confidence. With accurate financial visibility and industry-specific guidance, contractors can scale operations, improve margins, and reduce risk across their project portfolio.

How Construction Accounting Differs from Traditional Accounting

Construction accounting diverges from traditional business accounting because financial performance is driven by individual projects rather than continuous product or service sales. Each contract functions as its own economic unit with distinct costs, timelines, risks, and billing terms. As a result, contractors must track revenue, costs, and profitability at the job level while simultaneously managing company-wide financial health across multiple active projects. This project-centric structure introduces accounting requirements that are far more complex than those in most industries.

Project-based revenue and cost tracking.

In traditional accounting environments, costs and revenues are recorded by department, product line, or period. In construction, however, every labor hour, material purchase, subcontractor invoice, and equipment charge must be assigned to a specific job and cost code. Profitability is measured per project, not just per period, and management decisions depend on accurate job-level financial data. Without disciplined job costing, contractors lack visibility into which projects generate or erode margins.

Long-term contract revenue recognition.

Most businesses recognize revenue when goods are delivered or services are performed. Contractors often perform work over months or years, requiring revenue to be recognized based on progress toward completion rather than billing or cash receipt. Methods such as percentage-of-completion align revenue with costs incurred and estimated total contract performance. This creates ongoing dependence on reliable cost-to-complete estimates and introduces volatility when project conditions change—dynamics rarely present in short-cycle industries.

Retainage and progress billing.

Construction billing structures also differ significantly from standard invoicing. Contractors typically bill periodically based on a schedule of values reflecting work completed, while customers withhold retainage—commonly five to ten percent—until substantial completion. This means earned revenue, billed revenue, and collected cash rarely align. Accounting systems must therefore track underbillings, overbillings, and retainage receivables to accurately represent financial position and liquidity.

Decentralized jobsite operations.

Unlike centralized production or service environments, construction work occurs across multiple jobsites with distributed supervision, procurement, and labor reporting. Costs originate in the field and must flow reliably into accounting systems, often through project managers, foremen, and subcontractor documentation. This decentralization increases the risk of delayed or incomplete cost capture and requires tighter integration between operations and accounting than most industries demand.

Together, these structural differences make construction accounting a specialized discipline requiring industry-specific systems, reporting, and financial oversight. Contractors that adopt accounting practices aligned with project economics gain clearer margin visibility, stronger cash control, and more reliable financial reporting across their portfolio of work.

Key Financial Challenges Contractors Face

Contractors operate in a financial environment where profitability depends on estimating accuracy, project execution, and disciplined financial management across multiple simultaneous jobs. Even well-run construction companies can experience significant earnings volatility because revenue, costs, and cash flow are tied to long-term contracts and field performance rather than stable recurring sales. The following financial challenges are among the most common drivers of contractor risk and performance variability.

Cash flow volatility.

Construction cash flow rarely aligns with profitability. Projects often require upfront labor, materials, and subcontractor payments months before corresponding billings are collected. Retainage further delays cash receipts, while seasonal slowdowns or project timing gaps can create sharp liquidity swings. Rapid growth can intensify these pressures as working capital becomes tied up across multiple projects. Without project-level cash forecasting and disciplined billing practices, contractors may face shortages despite strong backlog and reported profits.

Margin fade and cost overruns.

A project that begins with healthy estimated margins can erode over time due to labor inefficiencies, material price changes, subcontractor performance issues, weather delays, or scope growth. Because costs accumulate gradually, margin deterioration—often called margin fade—may go unnoticed until late in the project if cost-to-complete estimates are not regularly updated. Cost overruns on a few large jobs can materially impact company-wide profitability, particularly when multiple projects experience similar pressures.

Inaccurate job costing.

Reliable job costing is essential for understanding project performance, yet many contractors struggle with delayed cost entry, inconsistent cost codes, or incomplete allocation of burdens such as payroll taxes, equipment ownership, and supervision. When job cost data is inaccurate, reported margins become misleading and estimating feedback loops break down. Contractors may continue bidding work based on flawed historical performance, perpetuating underpricing and profit variability.

Billing versus revenue timing gaps.

Construction accounting separates three distinct measures: revenue earned based on progress, amounts billed to customers, and cash collected. These rarely occur simultaneously. Underbillings arise when revenue exceeds billings, signaling potential cash strain, while overbillings indicate advance billing relative to progress. Misalignment between billing and revenue recognition can distort financial statements and obscure project performance if not reconciled through accurate WIP reporting.

Compliance and tax complexity.

Contractors face layered regulatory and tax requirements uncommon in most industries. Long-term contract tax methods, multi-state taxation tied to jobsite locations, sales and use tax on materials and services, payroll compliance for field labor, and industry-specific reporting requirements all increase complexity. Larger contractors may also encounter government contract rules, prevailing wage compliance, or bonding-driven financial reporting standards. Navigating these obligations while maintaining operational efficiency requires specialized accounting expertise.

Together, these challenges explain why construction companies rely on industry-focused accounting systems and advisors. Contractors that implement accurate job costing, disciplined WIP processes, and proactive cash and tax planning gain earlier visibility into risks, more stable margins, and stronger financial control across their project portfolio.

Job Costing and Project Cost Tracking

Accurate job costing and project cost tracking are essential for construction company owners who want to maintain profitability, control expenses, and make informed decisions across every project. Without a clear understanding of costs as they occur, even profitable projects on paper can erode margins in practice. By implementing a structured approach to tracking labor, materials, equipment, and subcontractor expenses, construction companies can gain real-time insights into project performance and identify opportunities to improve financial outcomes.

A foundational element of effective job costing is the use of cost codes and cost categories. These tools allow companies to organize expenses by project, task, or department, making it easier to monitor spending and compare actual costs against budgets. Categorizing costs accurately ensures that all aspects of a project—from labor hours to materials and equipment—are captured and evaluated, providing visibility into areas that may be over- or under-performing.

Labor, materials, equipment, and subcontractor allocation is another critical component of project cost tracking. By assigning costs to the appropriate categories and tracking them in real time, construction owners can understand where resources are being consumed and how they contribute to overall project costs. This level of detail helps identify inefficiencies, optimize scheduling, and prevent cost overruns before they impact the bottom line. Accurate allocation also supports more precise bidding and estimating for future projects, helping companies maintain consistent margins.

Real-time job profitability tracking enables construction company owners to assess financial performance as projects progress rather than waiting until completion. By monitoring revenues and expenses continuously, owners can quickly detect deviations from budgeted expectations, adjust resources, or implement corrective actions to protect margins. This proactive approach reduces the likelihood of surprises and strengthens financial control over multiple concurrent projects.

Variance analysis and margin fade detection are essential for identifying trends that could erode profitability. Comparing estimated costs to actual expenditures highlights areas where the project may be underperforming, whether due to labor inefficiencies, material waste, or subcontractor issues. Detecting margin fade early allows construction companies to take corrective measures, improve forecasting accuracy, and implement best practices across future projects.

When combined, cost coding, precise allocation, real-time tracking, and variance analysis provide construction owners with a comprehensive view of project financial health. This structured approach to job costing not only protects profitability but also supports strategic decision-making, enhances operational efficiency, and positions construction companies for sustainable growth in a competitive market.

Work-in-Progress (WIP) Reporting

The WIP schedule is the financial backbone of a construction business and the most critical part of a company’s financial statements when presented to outside parties. When updated in a timely manner, the WIP schedule allows you to see a job’s current profitability, projected profitability at completion, how jobs are progressing compared to budget, current progress billings, and the current backlog. It can provide real-time feedback, which allows for an understanding of what is going well and what isn’t. Contractors who know and analyze this information regularly can make more impactful course corrections, which may involve various modifications to strategy for completing the project, such as increases or decreases in the amount of equipment and resources allocated, timeline modifications, earlier identification and approval of change orders, etc.

But problems often arise with small and medium-sized contractors when WIP reports are not designed with enough automation built into the process. As a result, the WIP reports are put off for weeks or months at a time, delaying their data analysis and significantly limiting the ability to identify problems early enough to make meaningful changes. This scenario results in more “loss jobs” and lower margins on profitable jobs. .At best, what would have been a good year for the contractor becomes an okay year. At worst, an okay year turns into a loss year, jeopardizing bonding and banking relationships.

Delayed WIP reporting also frequently impacts cash flow, as a contractor may be consistently underbilled when progress is compared to billings, in which case the contractor may end up essentially financing the job for the project owners. Having the most up-to-date information will allow the contractor to monitor billing and cost issues as they arise and take corrective action in real time.

Improve Your WIP Reporting

A few simple strategies may help your organization improve the timeliness of WIP reporting:

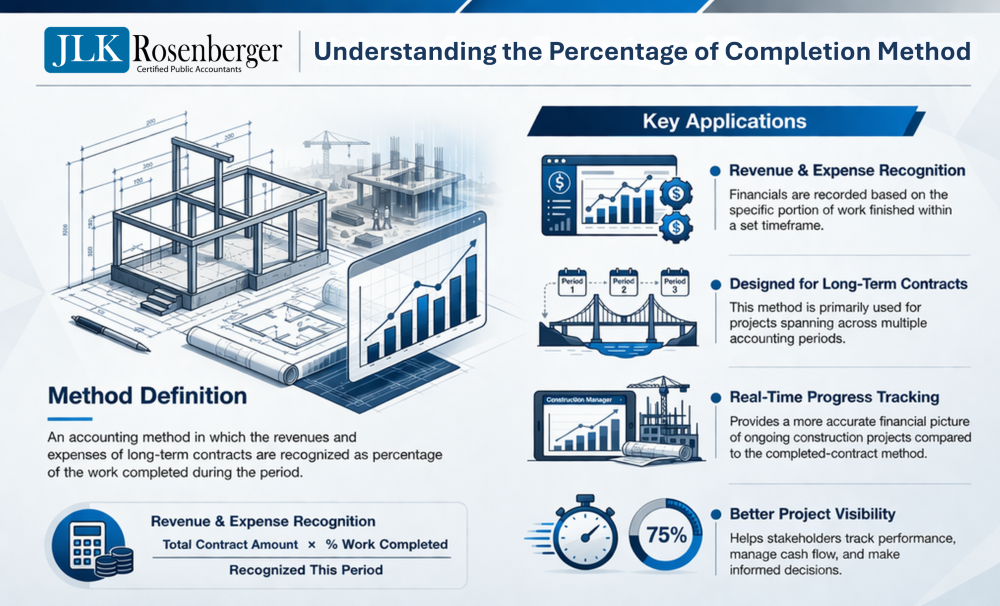

Revenue Recognition for Construction (ASC 606 / Percentage of Completion)

Revenue recognition under ASC 606 and the percentage-of-completion method is a critical component of financial management for construction company owners. Accurate recognition ensures that revenue and profits are reported in alignment with the work performed, provides a clear picture of project performance, and supports compliance with accounting standards. Misapplication of revenue recognition principles can distort financial statements, affect cash flow projections, and undermine decision-making.

The choice between the percentage-of-completion method and the completed-contract method is central to construction revenue recognition. The percentage-of-completion approach recognizes revenue and gross profit as work progresses, providing a real-time view of project performance and helping contractors manage cash flow, labor, and materials effectively. In contrast, the completed-contract method defers revenue recognition until the project is finished, which may be appropriate for short-duration projects or when estimating costs and outcomes is highly uncertain. Understanding the implications of each method allows construction owners to align accounting practices with operational realities and project risk profiles.

Contract modifications and change orders must be carefully evaluated under ASC 606 to determine how they impact revenue recognition. Approved change orders often result in additional contract revenue, but the timing and measurement of that revenue depend on the nature of the modification and its impact on project performance obligations. Proper accounting for contract changes ensures that financial statements reflect the true economic activity of the project and reduces the risk of overstating or understating revenue.

Claims and variable consideration present additional complexity in construction revenue recognition. Uncertainties such as disputed work, potential penalties, or bonus incentives must be assessed to determine whether they should be included in recognized revenue and how they should be measured. ASC 606 requires that variable consideration be estimated using a probability-weighted or most-likely approach, with recognition constrained to amounts that are reasonably assured. Applying these principles carefully helps contractors account for revenue realistically while maintaining compliance with accounting standards.

By implementing structured processes for applying the percentage-of-completion method, managing contract modifications, and evaluating claims and variable consideration, construction companies can achieve accurate and timely revenue recognition. This approach not only ensures compliance with ASC 606 but also provides owners with actionable insights into project profitability, cash flow, and long-term financial planning. Proper revenue recognition practices support more informed decision-making, reduce risk, and strengthen overall business performance

Tax Saving Opportunities

The Energy Efficient Commercial Buildings Deduction is available to commercial property owners and to those primarily responsible for designing qualifying facilities. To claim the deduction, projects must either involve new construction that incorporates approved energy efficient systems or retrofit existing buildings with eligible upgrades. Qualifying components may include interior lighting, HVAC systems, hot water heaters, and improvements to the building envelope. Importantly, these systems must achieve specific reductions in energy use, as defined by ASHRAE Standard 90.1-2019, to meet eligibility requirements.

The amount of the deduction that can be taken depends on two factors: the amount of energy saved and whether the prevailing wage and apprenticeship (PWA) requirements were met when constructing the energy efficient building. The savings amount (indexed for inflation) is $.50 per square foot, with 25% energy savings with an additional $.02 per square foot when savings exceed 25%. The maximum is $1.00 per square foot for a building with a 50% or greater energy deduction. When PWA requirements are met, the maximum benefit increases to 5 times the base savings per square foot.

To claim the credit, a study of the project must be completed by a third party to determine the applicable energy savings. Typically, IRS-approved software will be used to model energy performance and compare the updates against those of reference buildings. The third-party will also physically visit to verify the improvements meet the required standards. Finally, they will issue the necessary documentation, including the certification needed to claim the deduction.

Work Opportunity Tax Credit (WOTC)

This federal tax credit is available to construction companies that hire workers from certain disadvantaged groups. There are ten eligible groups, including certain veterans, ex-felons, designated community residents, summer youth employees, supplemental security income individuals, and long-term family assistance recipients. To be eligible, workers hired from eligible groups must be certified by a state workforce agency. Only eligible wages paid to certified workers before December 31, 2025, qualify.

Typically, the credit equals 40% up to $6,000 of wages paid to a worker in the first year of employment who is certified as a member of a targeted group and performs at least 400 hours of service. The maximum credit amount is $2,400 per worker. A 25% rate applies to individuals who work less than 400 but at least 120 hours. It is important to note that the credit cannot be claimed on re-hired employees and can only be used to offset business income tax liability or Social Security taxes owed.

Section 45L Tax Credit

This federal tax credit of up to $5,000 per home is available to eligible contractors that substantially reconstruct or build new energy efficient homes. The amount of the credit depends on specifics such as the type of home, energy efficiency achieved, and date when leased or sold. The available credit by home type includes:

An eligible contractor is an individual who constructed the home, owned and had a basis in it during construction, and sold/leased it for use as a primary residence. In the case of a manufactured home, it is the person who produced the home and owned/had a basis in it during production. It is important to note if someone owns a home but hires a third party to construct it, then the person who hired the contractor is considered the eligible contractor. In all cases, a house that is not considered to have been acquired is used as a primary residence by a contractor.

R&D Credits for Construction Innovation

Construction companies and contractors can take advantage of the federal Research and Development tax credit. The projects that are most commonly eligible include design-build, construction manager at risk, design-assist, and certain plans and specifications. Other projects, such as routine plan and specification projects, simple or routine paving, milling, and grading work, are more difficult to qualify. Finally, repair, maintenance, or warranty projects, labor-only, and projects are undertaken on a time and materials basis are usually ineligible.

Which Construction Activities Typically Qualify?

There are two primary activities that qualify:

Eligible Expenses

Specific expenses can be claimed, including wages, supplies, and third-party expenses.

What Construction Expenses Typically Qualify?

The most captured construction expenses include employee wages and certain subcontractor expenses related to engineering or direct support activities, such as testing and surveying.

Documentation

Ensuring the proper documentation is available to substantiate expenses claimed is necessary. The typical documentation which may be evaluated includes employee rosters, payroll records, job costing reports, Work in Progress (WIP), and contracts. Information may also be taken from other sources such as bid documents, calculations, change orders, erecting/picking plans, photographs, sketches, and more.

Multi-State and Sales Tax Issues

Multi-state operations create unique challenges for contractors, particularly when it comes to sales and use tax compliance. Businesses that work across state lines must navigate a complex web of rules regarding nexus, apportionment, jobsite taxation, and varying state tax structures. Failing to properly manage these obligations can lead to significant penalties, interest, and unexpected tax liabilities, making proactive planning and compliance essential for contractors operating in multiple jurisdictions.

A foundational concept in multi-state taxation is nexus, which determines whether a business has a sufficient presence in a state to trigger tax obligations. Nexus can be established through physical presence, such as offices, warehouses, or job sites, as well as economic presence, including sales volume or contractual relationships. Once nexus is established, contractors must understand how to apportion income and apply the correct state tax rules, ensuring that revenue is accurately reported and taxed according to each jurisdiction’s requirements.

Jobsite state taxation adds another layer of complexity for contractors. Many states impose taxes based on where the work is performed rather than where the company is headquartered, requiring careful tracking of project locations and related expenses. Understanding which states tax labor, materials, and services differently is crucial to avoid misreporting and to ensure compliance with local regulations.

Contractor sales and use tax obligations further complicate multi-state operations. Depending on the state, contractors may be responsible for collecting and remitting tax on materials, equipment, or subcontracted services. Misclassifying taxable versus exempt items or misunderstanding state-specific rules can lead to audits and financial exposure. Additionally, gross receipts taxes in certain states may apply to total revenue rather than profits, requiring contractors to factor these obligations into project pricing and financial planning.

Effectively managing multi-state and sales tax issues requires a combination of accurate record-keeping, careful planning, and a thorough understanding of state-specific rules. Contractors must monitor changes in tax laws, track project locations, properly classify taxable transactions, and apply apportionment rules consistently. By taking a proactive approach to multi-state taxation, businesses can reduce risk, maintain compliance, and make more informed financial decisions across all jurisdictions in which they operate.

Progress Billing and Cash Flow Forecasting

Progress billing and cash flow forecasting are critical tools for construction company owners seeking to maintain healthy finances and ensure project stability. Effective management of billing and cash flow enables contractors to align revenue with project costs, reduce financial risk, and make informed decisions about resource allocation and growth. Without a structured approach, projects can appear profitable on paper while creating cash shortfalls that jeopardize operations and overall business performance.

A key component of progress billing is the design of a schedule of values. This document breaks down the total contract amount into specific line items, allowing contractors to track work completed and bill accordingly. A well-structured schedule of values provides transparency for clients, supports accurate billing, and ensures that revenue is recognized in alignment with project progress. By clearly defining the allocation of costs, contractors can minimize disputes and maintain steady cash inflows throughout the project lifecycle.

Billing timing strategies play an equally important role in cash flow management. Determining when to submit invoices, how to sequence billings for milestones, and coordinating with payment terms can have a significant impact on liquidity. By carefully planning billing intervals, contractors can reduce delays in payments, maintain sufficient working capital for labor and materials, and prevent cash flow bottlenecks that can disrupt project execution.

Retainage is another factor that directly affects cash flow. Many contracts withhold a portion of payment until project completion or the fulfillment of specific milestones. Understanding the impact of retainage on day-to-day operations allows contractors to anticipate funding gaps, manage temporary financing needs, and structure projects to minimize financial strain while ensuring compliance with contractual obligations.

Cash flow projection models provide a forward-looking view of financial health by estimating future inflows and outflows. These models consider scheduled billings, expected payments, ongoing costs, and retainage, allowing contractors to plan for staffing, equipment, and material needs without compromising liquidity. Accurate projections also support decision-making around new project opportunities, capital investments, and operational adjustments, providing a roadmap for sustainable growth.

By integrating schedule of values design, billing timing strategies, retainage management, and robust cash flow projection models, construction companies can achieve predictable revenue streams and maintain financial control. This structured approach not only protects profitability on individual projects but also strengthens the overall financial position of the business, enabling owners to scale operations, pursue strategic opportunities, and navigate complex projects with confidence.

Top Cash Flow Killers

Below are the top cash flow killers that construction company owners and managers need to guard against to ensure financial vitality. These include:

Overhead Allocation and True Job Profitability

Understanding overhead allocation and true job profitability is essential for construction company owners who want a clear picture of project performance and sustainable margins. Many projects may appear profitable on the surface, but without properly accounting for all indirect costs, including office support, field supervision, and equipment expenses, actual profitability can be significantly overstated. By accurately allocating overhead, contractors gain a realistic view of each project’s contribution to the company’s bottom line and can make more informed decisions about pricing, resource deployment, and growth strategies.

A critical component of overhead allocation is the identification and assignment of burden and indirect costs. These include expenses such as administrative salaries, office rent, utilities, insurance, and other costs that are not directly tied to a specific project but are necessary for the business to operate. Proper allocation methods ensure that these costs are fairly distributed across all jobs, providing a true reflection of profitability and helping owners understand which projects are genuinely contributing to the company’s financial health.

Differentiating field versus office overhead is another important factor in assessing true job profitability. Field overhead includes site supervision, temporary facilities, safety programs, and on-site administrative support, while office overhead covers corporate functions, accounting, human resources, and management. Recognizing the distinct impact of these categories allows contractors to allocate resources efficiently, optimize staffing, and control costs in both operational and administrative areas.

Equipment cost recovery also plays a significant role in understanding real project profitability. Construction equipment represents a substantial investment, and costs such as depreciation, maintenance, fuel, and operator wages must be accounted for accurately. Assigning equipment costs to the appropriate jobs ensures that project pricing reflects the true resource consumption and prevents profits from being overstated due to unrecognized equipment burdens.

Failing to allocate overhead properly can result in under-absorbed overhead, creating hidden risks for contractors. Projects that appear profitable without full allocation may, in reality, be generating losses, eroding overall margins, and compromising cash flow. By systematically tracking and assigning overhead costs, construction company owners can detect these issues early, make adjustments to project pricing or resource allocation, and ensure that all jobs contribute appropriately to the organization’s financial performance.

By integrating burden and indirect cost allocation, field and office overhead distinctions, equipment cost recovery, and monitoring under-absorbed overhead, construction companies can achieve a comprehensive understanding of true job profitability. This approach enables owners to price projects accurately, manage resources effectively, and sustain healthy margins, ultimately supporting long-term growth and operational stability.

Change Orders, Claims, and Disputes Accounting

Change orders, claims, and disputes are a normal part of construction projects, but without proper accounting and management, they can significantly impact profitability and cash flow. Construction company owners need a clear framework for tracking, documenting, and recognizing revenue from these items to ensure financial accuracy and minimize risk. Effectively managing change orders and claims not only protects margins but also strengthens client relationships and reduces the potential for disputes that can disrupt project execution.

A critical aspect of managing change orders is distinguishing between approved and unapproved items. Approved change orders represent additional work that has been formally accepted by the client and can be recognized as revenue once performed, while unapproved change orders carry risk and should not be recorded until formal approval is obtained. Accurate tracking of these distinctions helps contractors avoid premature revenue recognition and ensures that project financials reflect actual agreements with clients.

Claims accounting treatment is another essential consideration. Claims related to delays, unforeseen conditions, or contract adjustments require careful documentation and appropriate accounting recognition. Construction companies must evaluate the likelihood of collection and determine how to reflect claims in financial statements without overstating revenue. Proper treatment of claims ensures compliance with accounting standards and provides a realistic view of project performance.

Margin and revenue timing risks are inherent in projects with change orders and claims. Delays in approval or disputes can postpone revenue recognition, impacting cash flow and distorting profitability metrics. By monitoring these timing risks closely, contractors can plan resources, adjust forecasts, and take proactive steps to mitigate financial exposure. This discipline helps maintain steady cash flow and ensures that project performance is accurately reflected in reporting.

Documentation best practices are vital for protecting the company in the event of disputes. Detailed records of change order requests, approvals, communications, and supporting evidence for claims provide a clear audit trail and support financial reporting accuracy. Strong documentation also enhances the company’s ability to resolve conflicts efficiently, demonstrate compliance with contract terms, and preserve client trust.

By combining disciplined tracking of approved and unapproved change orders, careful claims accounting, management of margin and revenue timing risks, and robust documentation practices, construction company owners can maintain control over project financials. This integrated approach ensures that all adjustments, disputes, and claims are properly reflected in accounting records, protects profitability, and strengthens overall project and business performance.

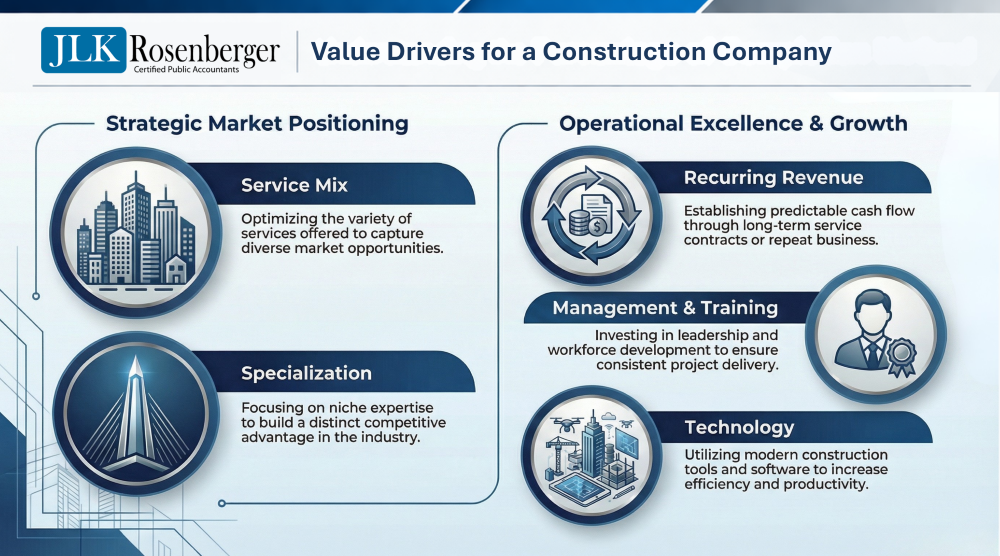

Profitability and Margin Improvement

Profitability and margin improvement are critical priorities for construction and project-based organizations that want to remain competitive while managing rising costs, labor constraints, and fluctuating market demand. Even companies with strong revenue growth can struggle with inconsistent margins if project performance, estimating accuracy, and bidding strategies are not carefully evaluated. A comprehensive profitability review helps organizations understand where margins are being gained or lost and provides a clear path to improving financial performance across current and future projects.

One of the most important steps in improving profitability is conducting detailed job margin diagnostics. This process involves analyzing completed and ongoing projects to determine which types of work consistently produce strong margins and which tend to erode profitability. By reviewing job costs, labor efficiency, subcontractor performance, change orders, and project management practices, organizations can identify patterns that impact financial outcomes. Job margin diagnostics also help uncover operational issues such as underperforming crews, scheduling inefficiencies, or poorly defined scopes of work that may be reducing profitability. With these insights, companies can make better decisions about project selection, operational improvements, and resource allocation.

Another key component of margin improvement is evaluating the relationship between estimating and actual project costs. Many margin issues originate during the estimating phase when project budgets are developed using assumptions that may not fully reflect real-world conditions. Estimating versus actual cost analysis compares initial estimates with final job costs to determine where discrepancies occur. These reviews often reveal recurring issues such as underestimated labor hours, inaccurate material pricing, or overlooked project complexities. By identifying these gaps, organizations can refine their estimating processes, improve cost forecasting, and develop more accurate bids for future projects. Over time, better alignment between estimates and actual costs leads to stronger margins and fewer financial surprises.

Bid strategy also plays a major role in overall profitability. Many firms focus heavily on winning projects but may not fully evaluate whether the projects they pursue are aligned with their operational strengths and margin expectations. Bid strategy optimization involves reviewing historical win rates, project profitability, and market conditions to determine the most effective pricing and bidding approaches. Organizations may discover that certain types of projects, contract structures, or clients consistently produce better outcomes. Adjusting bid strategies based on this analysis allows companies to focus on opportunities where they have a competitive advantage while maintaining healthy margins.

Closely related to bid strategy is project mix analysis, which evaluates the types of projects a company pursues and how those projects contribute to overall financial performance. Not all projects deliver the same level of profitability, and some may require more resources, risk, or management attention than others. By analyzing project size, complexity, location, contract type, and client relationships, organizations can develop a clearer understanding of which types of work generate the strongest returns. This analysis allows leadership to prioritize projects that align with their capabilities and long-term strategy while reducing exposure to lower-margin opportunities.

Succession, Exit, and Valuation for Contractors

Succession, exit, and valuation planning are critical considerations for contractors looking to secure the long-term success of their business, maximize value, and ensure a smooth ownership transition. Whether a business owner is preparing for retirement, considering a sale, or evaluating alternative ownership structures, understanding the key drivers of value and establishing a clear plan is essential to achieving both financial and operational goals. Without careful planning, contractors risk leaving value on the table or encountering disruption during ownership changes.

A fundamental aspect of contractor succession planning is understanding the factors that drive business valuation. Contractor valuation drivers often include revenue and profit trends, client diversification, backlog of work, operational efficiency, and the strength of management and field teams. By identifying and enhancing these value drivers, business owners can position their company to attract buyers, support internal transitions, or facilitate employee ownership structures. Clear insight into what influences valuation provides a roadmap for improving business performance and maximizing equity.

Ownership transition planning is equally important, as it outlines how leadership and ownership responsibilities will shift over time. Effective planning considers the timing of the transition, the role of key employees, tax and estate considerations, and the communication strategy for clients and staff. A well-structured plan helps ensure continuity, preserves client relationships, and maintains operational stability while preparing the business for a change in ownership.

For contractors exploring exit options, ESOPs and sale readiness strategies are increasingly relevant. Employee Stock Ownership Plans (ESOPs) offer a way to transfer ownership to employees while creating liquidity for the business owner, maintaining company culture, and incentivizing staff performance. Preparing a business for sale, whether to an external buyer or through an ESOP, requires a careful evaluation of financial records, contracts, operational processes, and legal structures to ensure the company is attractive to potential buyers and capable of sustaining long-term success.

Financial normalization is a key step in both valuation and exit planning. This process involves adjusting historical financial statements to reflect the true economic performance of the business, removing one-time or non-operational expenses, and standardizing owner compensation. Normalized financials provide a clearer picture of profitability, making it easier for buyers or stakeholders to assess value and for owners to make informed decisions about pricing, negotiations, and succession timing.

By addressing valuation drivers, ownership transition planning, ESOP and sale readiness, and financial normalization together, contractors gain a comprehensive approach to succession and exit planning. This integrated strategy ensures that the business is well-positioned for a smooth transition, maximizes value for the owner, and preserves the long-term health of the organization. Thoughtful planning allows contractors to approach succession and exit with confidence, minimizing risk while creating opportunities for continued growth and stability.

Increasing Bonding Capacity

Driving growth and profitability means leveraging opportunities when they arise. This often means submitting proposals for larger and more complex projects in the construction industry. However, larger opportunities frequently require contractors to have the proper bonding capacity. Bonds provide project owners with assurance that the contractor has both financial stability and the capability to complete a project. Without adequate bonding, contractors can lose out on larger projects, leaving them “boxed in” to smaller projects, which could slow growth. For this reason, many construction companies are interested in learning how to increase bonding capacity.

What Is Bonding Capacity?

Bonding capacity sets the ceiling on how much surety credit a construction company can secure at any given time. Sureties establish two key limits: a single project limit, which sets the highest bond available for an individual contract, and an aggregate limit, which caps the total value of bonded work a company can manage at once. These limits significantly impact a contractor’s ability to compete for larger contracts, qualify for public-sector projects, and build credibility with project owners.

How Sureties Determine Bonding Capacity

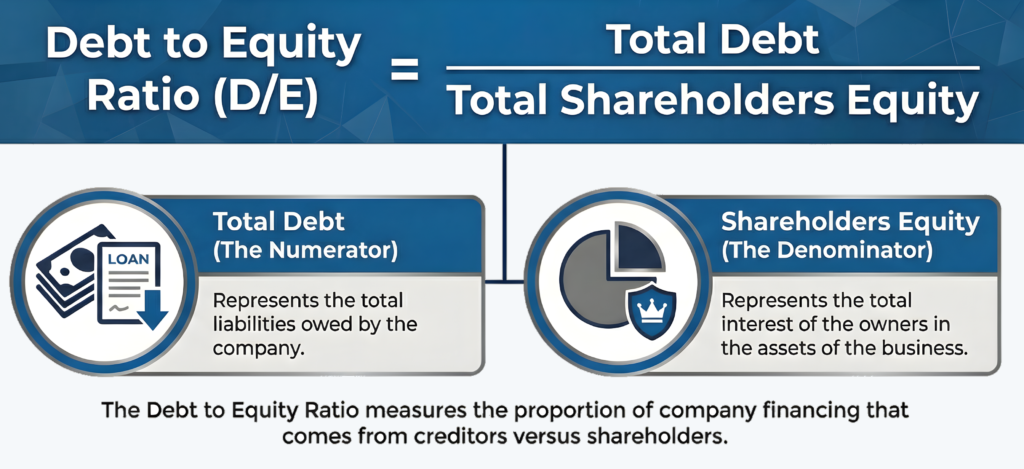

Sureties conduct a thorough financial review before issuing or increasing bonding limits. They assess liquidity, working capital, profitability, and debt levels to gauge financial health. Companies with strong cash reserves and manageable debt levels present lower risk, while those with inconsistent cash flow or excessive liabilities may face bonding restrictions.

Beyond financials, past performance plays a critical role. Sureties look at project history, assessing whether the contractor completes jobs on time, within budget, and without disputes. Delays, cost overruns, and legal claims can raise concerns, even for financially stable contractors.

Backlog management is also important. Contractors that take on too many bonded projects at once may appear financially stretched, limiting their ability to secure additional bonding. A well-managed backlog signals stability, showing that a company can scale responsibly without overextending resources.

Getting Started: Key Financial Statement Ratios

Contractors preparing to secure a bond or increase their bonding capacity should regularly evaluate these key financial ratios:

Construction companies operate in a high-risk financial environment where small accounting errors can compound across multiple projects and materially distort profitability. Many contractors rely on generic accounting practices that fail to capture project-level economics, leading to delayed loss recognition, weak cash flow visibility, and reduced bonding capacity. The following are among the most common construction accounting mistakes and how specialized construction CPAs help correct them.

Inaccurate Job Costing

Job costing is the foundation of construction profitability analysis, yet many contractors lack consistent cost codes, timely cost entry, or proper allocation of labor burdens, equipment, and subcontractor costs. When costs are recorded late or in the wrong categories, reported job margins become unreliable and estimating feedback loops break down. Contractors may continue bidding work based on flawed historical data, perpetuating margin erosion.

Construction CPAs design standardized cost structures, integrate payroll and equipment costing, and implement real-time cost tracking processes so project financial performance is visible and actionable throughout the job lifecycle.

Ignoring WIP Adjustments

The work-in-progress (WIP) schedule reconciles revenue recognized to costs incurred and billings, revealing overbillings and underbillings across projects. Contractors who treat WIP as a year-end exercise rather than an ongoing management tool often overlook margin fade, loss jobs, or billing imbalances until financial statements are finalized.

Construction CPAs establish monthly WIP procedures, validate cost-to-complete estimates, and ensure WIP adjustments are reflected in financial statements. Consistent WIP accuracy improves internal decision-making and strengthens surety confidence.

Misstated Revenue Recognition

Revenue recognition errors are common when contractors record revenue based solely on billings or cash receipts rather than progress toward completion. This can materially overstate or understate profitability depending on billing timing. Complexities increase when change orders, claims, or variable consideration are involved.

Specialized CPAs apply percentage-of-completion or completed-contract methods correctly, align revenue with project progress, and ensure contract modifications are accounted for properly under applicable accounting standards. Accurate revenue recognition stabilizes earnings and improves financial credibility with lenders and sureties.

Poor Overhead Allocation

Many contractors evaluate job performance using only direct costs, ignoring the true burden of field supervision, equipment ownership, insurance, and indirect labor. This understates total project cost and inflates perceived margins, masking underperforming work and mispricing bids.

Construction accounting advisors develop burden rates and overhead allocation models that distribute indirect costs appropriately across projects. This produces true job profitability metrics and more accurate estimating benchmarks.

Unapproved or poorly documented change orders create significant financial risk. Contractors may incur costs before approval, fail to track pending change orders separately, or recognize revenue prematurely. This leads to disputed billings, delayed collections, and margin uncertainty. CPAs can implement change-order tracking systems, separate approved and unapproved amounts in WIP, and ensure accounting treatment reflects contractual enforceability. Strong controls improve revenue reliability and dispute defense.