Feds Troubled with Insurance Industry Private Credit Concentration – Where’s the Beef?

Technological advancement brings greater capability to design sophisticated products, including financial products and instruments. In a relatively short period of time, the investment community has developed a superfluity of new and unique financial instruments, many of them with complex features. That evolution has raised the ire of state insurance regulators, and more recently, U.S. federal regulatory agencies, particularly within the private credit-backed marketplace. This article will address those concerns with key discussions regarding:

- Background events and history leading up to these concerns

- National Association of Insurance Commissioners’ (NAIC) response to changing investment products

- U.S. Treasury concerns with the insurance investment portfolios

- We summarize with recent and historical insurance regulatory mechanisms in place to proactively provide guardrails and buffer points to monitor and address potential impairment issues

Recent reporting by the Wall Street Journal has shed light on a corner of the insurance industry that is well understood by insiders but not as familiar to non-insurance readers and investors — the industry’s significant investments in private credit markets.

The insurance industry’s investments in private credit instruments have evolved over the past 15 to 20 years as sponsors within the pooled investment community have become more inventive, creating private credit instruments with unique characteristics.

These investments are attractive because they offer higher yields through a combination of illiquidity and risk. They also have the potential to expose companies to heavier default risk, which is the focus of recent attention.

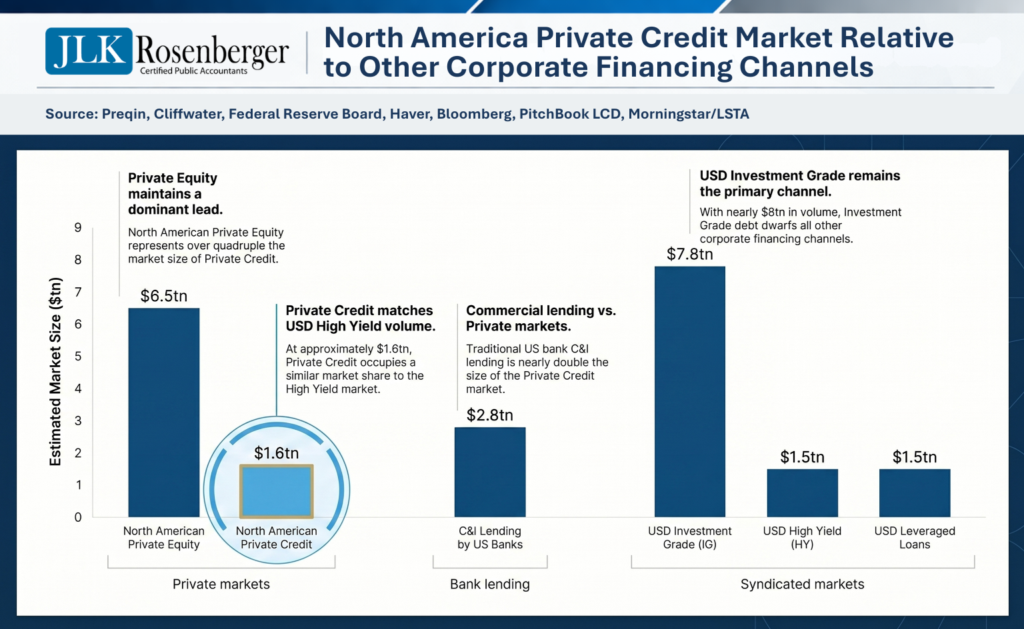

The industry’s investments today have shifted toward pooled investment vehicles centered on loans extended to businesses outside the commercial banking system, generally at attractive yields, commonly first-lien and senior-secured, and generally floating-rate around a wide spread to a reference rate. While these loans are made on the private market rather than within the banking system, it should not be assumed that they are low-quality. Many sophisticated lending groups consider private credit to be a superior funding source for many borrowing options.

In earlier years, large-scale private credit investment was the purview of just a few industries like insurance, which primarily invested in fixed income and established pooled investments that were likely to be publicly traded on exchanges and therefore normalized and accepted. But a confluence of factors, led by extremely low interest rates starting in 2022, has attracted non-industry investors to the private credit investment marketplace, such as pension funds, college endowments, and high-net-worth individuals, making institutional-caliber private credit more widely traded among a broad audience.

NAIC 2024 Report

The intensified interest in private credit investments gained velocity in 2024, when the NAIC published a study revealing that ratings on insurers’ private-credit investments were frequently inflated.

As a result, the NAIC report has raised concerns on the part of private-credit investors about the financial health of companies taking out private loans, and has also drawn scrutiny from the Treasury Department.

In May 2025, the NAIC pulled the report from its website and said it needed to “clarify its findings,” but the attention it drew has not diminished. As a result, NAIC and the insurance industry have some work to do to improve regulators’ and lawmakers’ understanding of the concept of private credit investment.

How Investments Are Rated for the Insurance Industry

Private credit investments account for about $1 trillion, or about 17%, of the invested assets held by life and annuity companies. Nearly half of that amount carries a private-letter rating, which is a letter grade rating on an investment that investors — including insurance companies — can obtain from a ratings firm.

In addition, at the behest of the insurance industry over the past decade, NAIC’s investment staff began assigning a risk score to private credit investments, just as it did for a bond’s public credit rating. But questions arose within NAIC about investment staff assigning risk scores to private credit instruments based on letter ratings from external ratings agencies, rather than evaluating the investments themselves.

To strengthen its oversight of the fixed income markets, the NAIC recently completed and implemented a long-standing project to revamp the entire analysis and reporting process for the fixed income facet of statutory reporting. This is a response to dramatic changes in the investment marketplace.

The Principle-Based Bond Project

Over the past 30-plus years, the investment marketplace has exploded with a remarkable palette of new and unique investment instruments. These financial instrument innovations precipitated the NAIC’s reassessment of its fixed-income benchmarks and reporting.

The NAIC’s Principle-Based Bond Project (or PBBP), which overhauled the statutory accounting principles for bond classification, has resulted in a more focused fixed-income analysis process for determining an instrument’s classification. This activity adds support to an improved oversight position if properly followed by insurance industry constituents and their investment advisors. The PBBP was finalized in 2024 and became effective on January 1, 2025. It has greatly refined how securities are defined and classified, which should potentially lead to better refinements in future security analysis and ratings.

Applying Standards That Fit the Private Credit Marketplace

A key perspective that cannot be dismissed is that anxiety over the private credit market is heavily influenced by standards normally applied to the equity side of financial markets. This anxiety has been further perpetuated by media coverage.

For years, the life and annuity side of the insurance industry has maintained the Asset Valuation Reserve (AVR), which functions as a separate buffer reserve providing a backstop if major fluctuations in the investment marketplace and economy negatively impact a life insurance entity’s portfolio. The AVR functions as a proactive credit loss reserve, developed formulaically and underpinning the investment portfolio, should a life insurance company experience downward pressure on its investment holdings. The AVR is a mandatory reserving methodology that all life insurers are required by NAIC to maintain.

Finally, the NAIC maintains a large investment analysis division, the NAIC Investment Analysis Office, comprised of:

- The NAIC Securities Valuation Office (SVO) analyzes and oversees the investment securities being purchased and held by the insurance community. This group assesses and is in charge of monitoring and assigning investments to NAIC credit ratings.

- The Structured Securities Group oversees RMBS and CMBS modeling and risk analysis.

These groups support the insurance regulatory system by maintaining an independent system of fixed-income review and analysis, and producing the NAIC security rating system used by all insurance carriers. These NAIC subdivisions utilize independent credit rating providers — S&P Global, Moody’s, Fitch, A.M. Best, Egan Jones, Kroll, Morningstar, etc. — to supplement their analysis, but have the final say over what is assigned for NAIC credit ratings.

The recent Wall Street Journal article, and others, have illuminated the concerns that many of these CRP-assigned ratings are running several notches higher than the NAIC would assign to private credit investments, along with the point that the insurance industry has a heavy concentration in private credit instruments. The rating notch issue is not terribly surprising, considering the regulatory intent focuses on conservatism and solvency, and rating agencies are paid for their rating services, yet must be monitored for potential bias.

Clearly, insurance regulators have experienced multiple situations over the years when carriers got loosey-goosey (to use a proper idiomatic expression) in chasing yield and left underwriting under the table. Foolish investing in a poorly backed or poorly studied private credit instrument could certainly impact impairment issues.

Is it systemic, though? The Treasury and SEC evidently have concerns that the heavy use of private credit investment in the insurance arena is concerning from a concentration perspective and could lead to a systemic situation should some form of a cascading default scenario occur.

As insurance industry participants, we are cognizant of this situation, but also have the built-in NAIC self-governance guardrails previously noted, which are continually monitored.

Treasury Department Oversight

Treasury Secretary Scott Bessent has reportedly been planning to initiate regular, sustained consultations with insurance regulators beginning in the second quarter of 2026.

While Treasury has no direct regulatory authority over the insurance industry, Treasury officials reportedly have discussed seeking feedback from regulators on a host of issues, including the consistency of private credit ratings, the liquidity of investments in private credit markets, the rising use of fund-level leverage, and the use of offshore reinsurance.

There is no discussion of the Treasury Department or any other federal agency asserting regulatory control over the insurance industry. Existing state-level regulatory control already accounts for insurance being one of the most heavily regulated industries in the country.

But the fact that discussions are being held at the federal level about the insurance industry’s activity in the private credit marketplace indicates the level of concern that has arisen.

Summary

Federal regulators have legitimate concerns as they have observed the heavy shift into private credit loan markets, in conjunction with the attention private credit is receiving in the general markets. The insurance regulatory community should welcome those concerns and open discussions. Recalling the history of the 1991 junk bond wave that created several life insurance company failures and the ensuing “runs on the insurers,” coupled with the 2008 global financial crisis and bailouts, brings back fresh memories to state and federal regulatory minds. The buzzword “systemic” starts to be tossed about, which inflames the fear (and the media).

Yet, the insurance industry comes well-armed to the discussion table with how it has proactively addressed historical market upheavals, implementing major programs to strengthen oversight and sedate the potential solvency impact. That self-governance toolkit includes:

- The Asset Valuation Reserve (AVR) emerged in the early 1990s to supplement and provide better cushioning effects in the event of future downturns in credit markets.

- Risk-based Capital (RBC) came into existence in 1993 (life) and 1994 (property and casualty) following the junk bond market turmoil, functioning as a risk management monitoring tool for state regulatory departments. For life insurers, approximately 80% of RBC is associated with asset and interest rate risk.

- The National Association of Life and Health Insurance Guaranty Associations was founded in the early 1980s to better coordinate the state-level guaranty associations that were initiated in the 1970s and 1980s with the objective of providing a secondary safety net to bail out policyholders of large-scale insurance entity failures. The property and casualty industry maintains similar state-based, non-profit organizations to accomplish the same task.

- Following the 2008 financial meltdown, the Owned Risk Solvency Assessment (ORSA) program was initiated beginning in 2015, with all states having implemented it by 2021. ORSA is a risk-management assessment facility following an enterprise risk management concept and is applicable to large life and property and casualty entities with $500 million of direct and assumed premium, or $1 billion in direct written and assumed premium if part of an insurance group.

- The aforementioned PBBP came online in 2025, providing strict definitions and refining what comprises a debt security, with particular emphasis on asset-backed investments. This project will put heavy responsibility on investment advisors to become knowledgeable and accountable regarding insurance investment criteria when selecting potential investments for their insurance clients.

All of these protective guardrails are solid backstops and buffer points to contain the industry from systemically running off the tracks. Yet they all fall in line behind the most common-sense guardrail. And that is clear and sensible underwriting of each credit (whether private or public) being considered for an insurer portfolio.

Conclusion

A key ending point – insurance boards should continually make certain their investment and financial management departments are vetting their investment advisor’s knowledge of insurance state rules, and in particular, how the credit meets the NAIC PBBP details. Questioning advisors about how a suggested investment clearly fits the PBBP criteria and expecting an educated, knowledgeable response should be taken very seriously. Complacency in this important internal management facet is purely a control slip. If that advisor is simply pushing product, consider engaging a vetted insurance-knowledgeable partner.

We’re Here to Help

If you would like to discuss your insurance company’s investment approach and the private credit market, contact your JLK Rosenberger team member, call 818-334-8646, or click here to contact us. We look forward to speaking with you soon.