Presidential Candidates’ Tax Plan Comparison

Americans will go to the polls on November 5, 2024, to elect the 47th President of the United States, and in terms of the nation’s tax policy, the stakes could not be higher.

Americans will go to the polls on November 5, 2024, to elect the 47th President of the United States, and in terms of the nation’s tax policy, the stakes could not be higher.

Both Vice President Kamala Harris, Democrat, and former President Donald Trump, Republican, have released tax plans which, predictably, could not be farther apart from the standpoint of tax and economic ideology – and in terms of who will pay and who will benefit the most.

Given the deep partisan divide that defines the relationship between presidents and Congress, no president can expect to achieve all their goals with a tax and economic plan. However, the major features of both Harris’s and Trump’s plans point to broad economic convictions that will undoubtedly shape the nation’s tax policy for the next four years.

Harris and Trump offer contrasting visions for the U.S. tax system. Trump’s plan favors tax cuts and deregulation, while Harris’s plan emphasizes increased taxation on the wealthy and expanded social programs. Understanding these proposals requires examining their key elements, impacts on various income groups and broader economic implications.

The following are highlights and analyses of what we know so far about Harris’s and Trump’s plans, understanding that these plans may change between now and Election Day.

Trump’s 2024 Tax Plan

Donald Trump’s tax plan for 2024 largely builds on the framework of his 2017 Tax Cuts and Jobs Act (TCJA). His proposals generally focus on:

- Tax Cuts for Individuals and Corporations: Trump proposes extending the tax cuts for individuals that were part of the TCJA, which are set to expire after 2025. These cuts reduced income tax rates across various brackets and aimed to stimulate economic growth through increased consumer spending and investment. His plan also includes further reductions in corporate tax rates from 21% (established by the TCJA) to potentially as low as 15%.

- Deregulation: Trump’s tax plan is closely linked with his broader deregulatory agenda. He argues that lower taxes will stimulate business investment and job creation, thereby boosting economic growth. This includes easing environmental and labor regulations that he believes stifle economic activity.

- Elimination of Estate Tax: Trump’s plan advocates for the complete elimination of the estate tax, which he argues will benefit small businesses and family farms. The loss of revenue to the federal government could be upwards of $25 billion annually.

Trump’s specific major proposals include:

- Permanence for the expiring individual provisions of the TCJA

- Permanence for the expiring estate tax provisions of the TCJA

- Permanence for the business tax phaseouts of the TCJA (100% bonus depreciation, R&D expensing and an EBITDA-based interest limitation)

- Lower the corporate tax rate to 20%

- Lower the corporate tax rate to 15%

- Exempt tips from income taxes

- Exempt Social Security benefits from income taxes

- Eliminate the green energy subsidies in the Inflation Reduction Act

- Raise current Section 301 tariffs on China to 60%

- Impose a universal tariff on all U.S. imports of 10% to 20%

Harris’s 2024 Tax Plan

Kamala Harris’s tax plan reflects her progressive stance on economic policy. Key elements include:

- Increased Taxes on the Wealthy: Harris proposes raising taxes on high-income earners and large corporations. Her plan includes increasing the top income tax rate for individuals earning over $400,000 to 39.6%, up from the current top rate of 37%. Additionally, she aims to increase capital gains taxes for those earning over $1 million annually, treating capital gains as ordinary income.

- Corporate Tax Increase: Harris’s plan proposes raising the corporate tax rate to 28%, reversing the TCJA’s reduction. She argues that this increase is necessary to ensure corporations pay their fair share and to fund public investments.

- Expansion of Social Programs: Harris’s tax plan is intertwined with her proposals for expanded social programs, including universal pre-K, increased funding for public education, and universal healthcare through an expanded Affordable Care Act or Medicare for All. These programs would be funded by increased taxes on the wealthy and corporations.

- Increased Estate Tax: Contrary to Trump’s plan, Harris supports expanding the estate tax, targeting large estates with higher rates to address wealth inequality.

Harris’s specific tax proposals include:

Business Tax Proposals

- Increase the corporate income tax rate from 21% to 28%

- Increase the corporate alternative minimum tax introduced in the Inflation Reduction Act from 15% to 21%

- Quadruple the stock buyback tax implemented in the Inflation Reduction Act from 1% to 4%

- Make permanent the excess business loss limitation for pass-through businesses

- Further limit the deductibility of employee compensation under Section 162(m)

- Increase the global intangible low-taxed income (GILTI) tax rate from 10.5% to 21%, calculate the tax on a jurisdiction-by-jurisdiction basis, and revise related rules

- Repeal the reduced tax rate on foreign-derived intangible income (FDII)

Individual, Capital Gains and Estate Tax Proposals

- Expand the base of the net investment income tax (NIIT) to include nonpassive business income and increase the rates for the NIIT and the additional Medicare tax to reach 5% on income above $400,000

- Increase top individual income tax rate to 39.6% on income above $400,000 for single filers and $450,000 for joint filers

- Tax long-term capital gains and qualified dividends at 28% (as opposed to 39.6% as in the Biden budget) for taxable income above $1 million and tax unrealized capital gains at death above a $5 million exemption ($10 million for joint filers)

- Limit retirement account contributions for high-income taxpayers with large individual retirement account (IRA) balances

- Tighten rules related to the estate tax

- Tax carried interest as ordinary income for people earning more than $400,000

- Limit 1031 like-kind exchanges to $500,000 in gains

- Exempt tipped income from income taxation for occupations where tips are currently customary

- Expand the Section 195 deduction limit for startup expenses from $5,000 to $50,000.

- Revive and make permanent the American Rescue Plan Act (ARPA) child tax credit (CTC) and increase the CTC for newborns to $6,000 in the first year of life

- Permanently extend the ARPA earned income tax credit (EITC) expansion for workers without qualifying children

- Provide a $25,000 tax credit for first-time homebuyers over four years

Comparative Analysis

General Economic Impact

An analysis of Trump’s plan by the Tax Foundation, a Washington D.C.-based think tank, identified the following broad impacts over a 10-year period:

- Loss of $1.3 trillion in tax revenues

- Loss of 0.2% long-term GDP

- Gain of 0.6% in long-term wages

- Loss of 387,000 full-time equivalent jobs

A similar analysis of Harris’s plan identified the following broad impacts over a 10-year period:

- Gain of $1.7 trillion in tax revenues

- Loss of 2.0% long-term GDP

- Loss of 1.2% in long-term wages

- Loss of 786,000 full-time equivalent jobs

Costly Proposals and Offsets

Both Harris and Trump include costly proposals in their tax and economic plans, which they intend to pay for with a combination of new taxes.

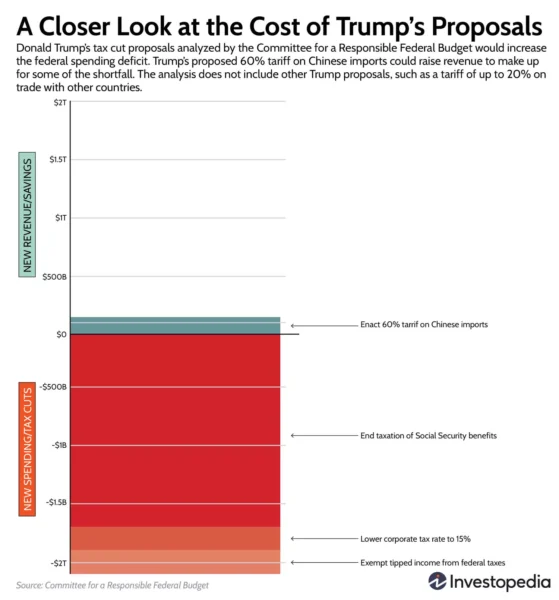

Trump’s tax plan includes an end to the tax on Social Security benefits. Social Security benefits were tax-free until 1984, when the Reagan Administration and Congress extended federal income tax to 50% of certain benefits, depending on a recipient’s total income. The Clinton Administration later boosted that percentage to 85%. If enacted, Trump’s proposal to end the federal taxation of Social Security benefits would reduce federal revenue by approximately $1.6 trillion, according to an analysis by the Committee for a Responsible Federal Budget (CRFB).

Trump’s other costly proposal would be a reduction in the maximum corporate tax rate from 21% to 15%, which would reduce revenue by approximately $200 billion.

Trump believes he can pay for those tax breaks and reduce the national debt by raising tariffs on foreign imports. He has proposed a 60% tariff on Chinese imports and tariffs of 10% to 20% on goods from other countries. Analyses by economists and think tanks cast doubt on whether Trump’s tariffs would pay for the proposed tax breaks, and they note that tariffs typically depress the economy by discouraging consumer spending and by triggering trade wars.

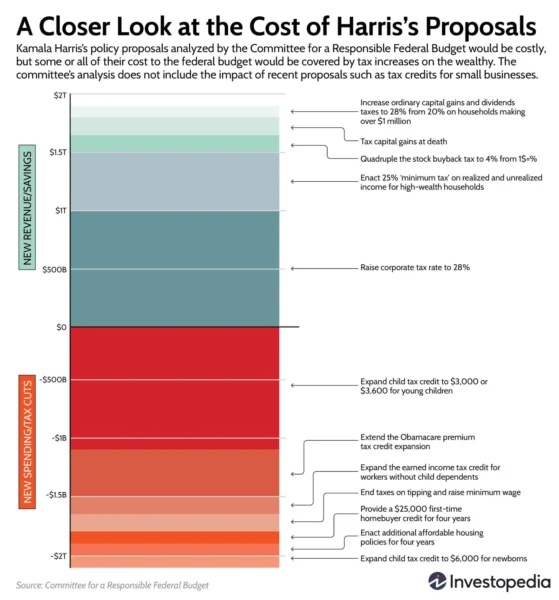

Harris’s costliest proposal would be an expansion of the child tax credit of up to $3,600 per year per child from its current level of $2,000, matching the temporary credit expansion implemented by President Joe Biden in 2021 as a COVID-19 relief measure. Additionally, Harris has proposed a $6,000-per-year credit for children in their first year of life.

Harris’s proposals would cost $1.2 trillion over 10 years, according to the analysis of the CRFB. Other items in her proposals that may push up the deficit include expanding the earned income tax credit for lower income workers, providing a $25,000 tax credit for first-time homebuyers, and expanding Affordable Care Act subsidies to reduce premiums for Americans who rely on the ACA for healthcare coverage.

Harris’s proposed tax hikes on the wealthy and corporations could cover most or all of those costs, according to the CRFB’s analysis. The most significant would be increasing the corporate tax rate to 28% from 20%, which would raise $1 trillion. The proposed 25% “billionaires tax” on income and unrealized investment gains for people with more than $100 million unrealized investment gains would raise an additional $500 billion.

The tax plans of Kamala Harris and Donald Trump for the 2024 presidential election reflect broad ideological differences regarding economic policy and fiscal responsibility. Ultimately, the effectiveness of each plan will depend on various factors, including implementation, economic conditions and the broader fiscal environment.

We’re here to help

If you have questions about the tax proposals outlined above or need assistance, JLK Rosenberger can help. For additional information, call us at 818-334-8625 or click here to contact us. We look forward to speaking with you soon.