R&D Tax Credits: Amortization Not Expensing

The federal Research & Development (R&D) tax credit available under IRC Section 41 (§41) is not only a useful tool to encourage innovation and development in the United States, but also represents a compelling savings opportunity today for many business owners across a wide range of industries. For many, the ability to reduce federal tax due immediately is what makes the incentive so attractive. Many states also offer R&D credit opportunities, such as California, which allows business owners to reduce corporate franchise tax and personal tax for the owners of pass-through entities.

In addition to the R&D tax credit available under §41, there is another tax incentive provided for research and experimental (R&E) costs under IRC Section 174 (§174). For many years, numerous companies have also been able to realize immediate savings by deducting eligible expenses incurred on an annual basis under §174. A common misunderstanding we are seeing today is that new legislation introduced as part of the Tax Cuts and Jobs Act (TCJA) has changed the tax savings available under § 41 through the R&D tax credit. The TCJA did make an important change that requires eligible R&E expenses to be amortized rather than immediately deducted beginning after December 31, 2021. This means that starting in 2022, the benefits available under §174 cannot be immediately taken but must now be realized over several years. Thus, while qualifying §41 expenses are now subject to the amortization requirements under §174, the R&D tax credit still offers powerful tax savings opportunities on an annual basis by allowing for an immediate reduction of the company’s federal income tax owed and allowing certain businesses, especially startups, to use the R&D tax credit to reduce the payroll tax. In addition, business owners can claim the R&D tax credit on amended returns up to three years back where any credits generated that cannot be used in a prior year can carry forward to offset income tax owed in the current year.

Another common misconception is that the requirements for eligibility and the allowable expenses under §41 and §174 is the same. When in fact, there may be additional R&E expenses allowed under §174, such as foreign, incidental, and production, compared to §41 where the requirements of the four-part test must be met for eligibility. The computation of allowable expenses is also unique under each provision. There are also still some unknowns regarding how to classify expenses that were generally considered ordinary and necessary. Thus understanding how to categorize and track certain expenses and the nuisances between §174 and §41 is very important in light of these new requirements.

This change has caused quite a bit of confusion and will certainly have an effect on corporate tax planning and projections. To help clients, prospects, and others, JLK Rosenberger has provided a summary of the key details to be aware of below.

What did the TCJA Change?

As mentioned above, the Tax Cuts and Jobs Act made several rule changes impacting how a company needs to treat R&E expenses claimed under §174. One key change is the timing of tax savings benefits under §174. Under new regulations, taxpayers can no longer immediately expense eligible costs, but must now capitalize the expenses over multiple years, five for domestic and 15 for foreign. In addition, amortization is required to start at the midpoint of the taxable year in which the expense is incurred. This means an eligible expense incurred in February would have to wait until July until amortization could begin. Another key change is how R&D expenses must be classified. Some exceptions include certain land and property acquisitions or improvement expenses relating to the allowance of depreciation under IRC Section 167 or allowance for depletion under IRC Section 611 and mineral rights. There was also a big change relating to the classification of software development expenses.

How is Software Development Impacted?

Historically, expenses related to software development could be expensed in the year paid or incurred with the option of also amortizing the expense over a period of 60 months from completion or 36 months from when it was placed in service. The TCJA change specified that costs related to software development must be treated as a §174 expense. As noted above, the requirements under §41 and §174 are different and this is especially true for software development. This means that in many instances, notably software developed primarily for internal uses, likely was included under §174 but may not be eligible for the R&D tax credit under §41. Thus, software development expenses regardless of if claimed for an R&D tax credit under §41 must still be amortized under §174.

How Does This Impact Us?

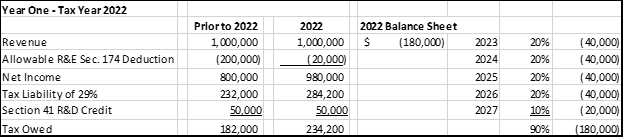

Most will now be forced to capitalize and amortize §174 R&E costs. Under prior regulations, a company that incurred $200,000 in eligible R&E §174 costs could expense the full amount in the year incurred. However, the TCJA change means these expenses must be taken over a longer period. In addition, since amortization starts at the midpoint of the year, the result is that a taxpayer can expense 10 percent in year one and the remaining 90 percent of the eligible R&E expense would be carried forward for the subsequent five years on the balance sheet. See the example below for specific details. For this example, we are assuming that the company has $200,000 in eligible R&E expenses, a tax liability of 29%, and generates a §41 R&D tax credit of $50,000.

Is a Form 3115 Required to Change Accounting Method?

Companies that previously deducted R&E expenses under §174 will be required to make a change in accounting method to permit the amortization of expenses. Previously taxpayers were required to submit IRS Form 3115 to change the accounting method. However, in IRS Revenue Procedure 2023-11, new automatic procedures were outlined specifically for those taxpayers changing accounting methods to comply with the new §174 amortization rules. This applies only to the first taxable year after December 31, 2021. Under these rules, rather than filing Form 3115, taxpayers simply need to include an informational statement when filing the original tax return, including:

- Name, Employer Identification Number (EIN), or Social Security Number (SSN).

- The beginning and ending dates of the first taxable year in which the change takes effect for the applicant (year of change).

- The designated automatic accounting method for this change.

- A statement of the type of expenditures included as specified R&E expenditures.

- The amount of specified R&E expenditures paid or incurred by the applicant during the year of change.

- A declaration that the applicant is changing its method of accounting for specified R&E expenditures to capitalize such expenditures to a specified R&E capital account and amortize such amount for five or 15 years depending on if the research was domestic or foreign. The amortization period must begin with the mid-point of the taxable year the expenses are paid or incurred. The applicant must also state the change is made on a cutoff basis.

For those seeking to change accounting methods after the first taxable year Form 3115 needs to be submitted in addition to a few of the requirements above.

What are the Next Steps?

It was widely expected that Congressional action would be taken to reverse this change, but it appears there will be no updates prior to the upcoming timely filing deadline. However, given the bipartisan support and push in Congress, it is likely that at a minimum a bill to extend this requirement may be forthcoming soon. The timing of this fix and if taxpayers will be able to apply it retroactively through an amended return is still unknown. For this reason, JLK Rosenberger recommends that impacted companies file for an extension and await further guidance. This prudent action will ensure taxpayers are in an optimal position should a reversal pass. In the meantime, it is also important to understand and track §174 expenses should a legislative solution not be implemented in the immediate future.

We’re Here to Help

The change to IRC Section 174 is complicated. For this reason, it is essential to consult with a qualified advisor who can assess the situation and determine how you will be impacted. If you have questions about the information outlined above or need assistance with an R&D credit, JLK Rosenberger can help. For additional information, call 949-860-9902 or click here to contact us. We look forward to speaking with you soon.